The Future of Banking: How Digital Banking Units (DBUs) are Revolutionizing Financial Access in 2026v

If you’ve walked into a bank recently, you might have noticed something different. The long queues for basic tasks like updating a passbook or depositing a cheque are slowly vanishing. In their place, a new era of "Phygital" banking is emerging.

As we navigate through 2026, the buzzword in the financial sector isn't just "Online Banking"—it’s Digital Banking Units (DBUs). But what does this mean for the average person, and how is it changing the way we look up an IFSC code or manage our savings?

What Exactly is a Digital Banking Unit?

A Digital Banking Unit is essentially a specialized fixed-point business hub equipped with interactive digital infrastructure. Think of it as a "Smart Bank" branch. Unlike a traditional branch with marble counters and glass partitions, a DBU is paperless, efficient, and largely self-service.

Key services offered by DBUs include:

Instant account opening via e-KYC.

Digital grievance redressal.

Instant issuance of debit cards.

Paperless loan applications for MSMEs and individuals.

Why This Matters for the "IFSC Generation"

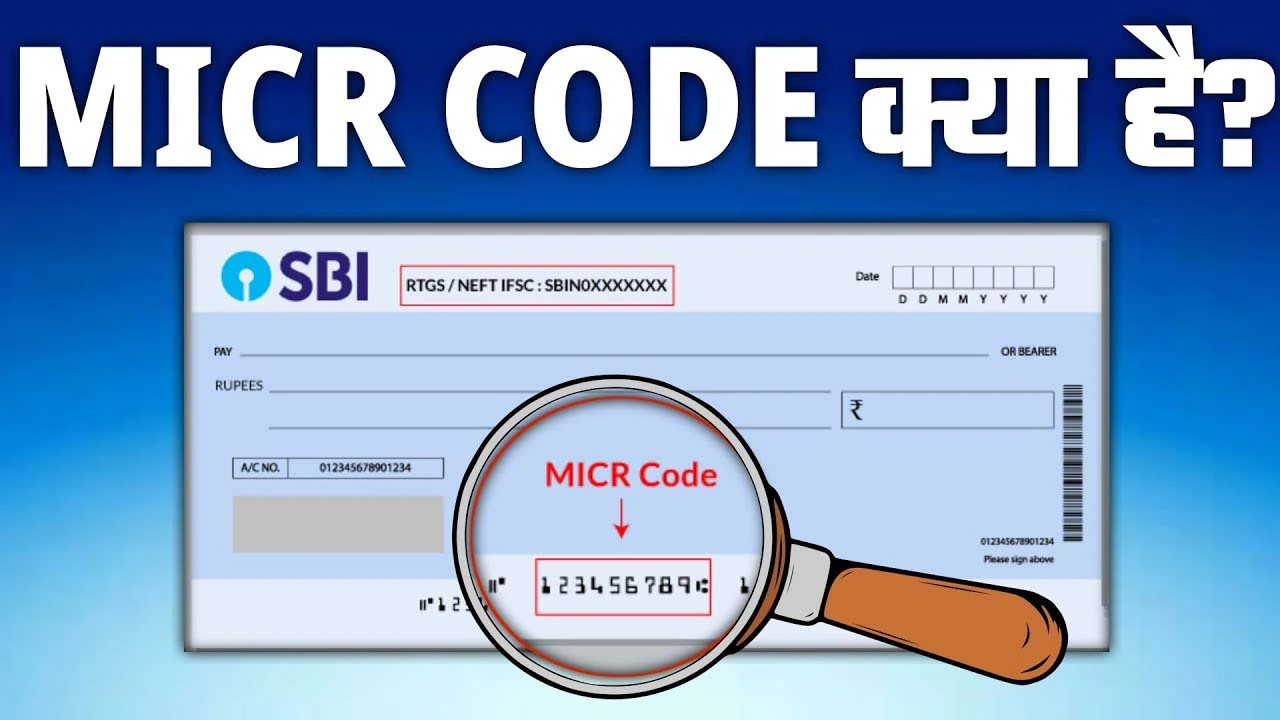

For years, we’ve relied on websites like IFSC Code Master to navigate the complex web of bank branches. However, as banks consolidate and physical branches transform into digital hubs, the technical backbone—the IFSC and MICR systems—is becoming more integrated with real-time AI tracking.

In 2026, a DBU allows you to perform inter-bank transfers (NEFT/RTGS) with higher security layers than ever before. While the IFSC remains your digital address, the DBU ensures that the transaction is verified via biometric or behavioral AI, reducing the risk of "manual entry" errors.

The Human Touch in a Digital World

Many people worry that "digital" means "impersonal." But the trend in 2026 is actually the opposite. Banks are using AI to analyze your spending habits not just to sell you products, but to offer financial wellness.

Imagine a DBU kiosk that doesn't just show your balance, but warns you: "Hey, your electricity bill is 20% higher this month—would you like to see a comparison of energy-saving tips?" That is the human-centric approach that modern finance is taking.

3 Tips to Stay Financially Secure in the Digital Age

Verify Before You Transfer: Even with high-tech DBUs, always double-check the IFSC code and branch name. A small typo can still lead to a temporary digital headache.

Embrace e-RUPI and CBDCs: The Central Bank Digital Currency (CBDC) is becoming mainstream. Using these digital tokens via DBUs can make your transactions near-instant and remarkably cheap.

Monitor Your Digital Footprint: With paperless banking, your data is your currency. Use two-factor authentication (2FA) for every financial app you own.

The Bottom Line

The transition from traditional brick-and-mortar branches to Digital Banking Units is more than just a tech upgrade; it’s a democratization of finance. Whether you are a small-town entrepreneur or a city-based professional, the barriers to high-end banking are falling.

The next time you search for an IFSC code or look to open a new savings account, remember that you aren't just looking for a bank—you're looking for a digital partner.